Parametric insurance policies pay based on pre-agreed thresholds like the magnitude and/or location of an earthquake. Some countries benefit from rapid payouts using this type of insurance.

By Mario A. Salgado-Gálvez, ERN International, Mexico City, Mario Ordaz, ERN International, Mexico City, and Instituto de Ingeniería, Universidad Nacional Autónoma de México, Mexico City, Shri Krishna Singh, Instituto de Geofísica, Universidad Nacional Autónoma de México, Mexico City, Xyoli Pérez-Campos, Instituto de Geofísica, Universidad Nacional Autónoma de México, Mexico City, Benjamín Huerta, ERN International, Mexico City, Paolo Bazzurro, RED – Risk, engineering + Development, Pavia, Italy, and Ettore Fagà, RED – Risk, engineering + Development, Pavia, Italy

Citation: Salgado-Gálvez, M.A. Ordaz, M., Krishna Singh, S., Pérez-Campos, X., Huerta, B., Bazzurro, P., Fagà, E., 2023, Developing new parametric insurance models for Caribbean and Central American countries, Temblor, http://doi.org/10.32858/temblor.303

Este artículo también está disponible en español.

When an earthquake hits, insurance claims follow. Traditional insurance payouts are based on the losses the insured party actually suffered, but for large earthquakes, this can be problematic because determining the actual losses for multiple policyholders can be a slow process. Thus, parametric insurance solutions can be used instead. Parametric insurance solutions not only provide faster payouts (within days of a quake) but can also be customized to the needs of the insured.

Because of the rapid payouts, some governments prefer the approach to earthquake insurance that parametric insurance provides. In 2007, 16 Caribbean countries formed the Caribbean Catastrophe Risk Insurance Facility (CCRIF), which was the first multinational insurance pool in the world. To date, 19 Caribbean and three Central American governments are members of CCRIF. Our research group recently updated the earthquake risk models for these countries (Salgado-Gálvez et al., 2023).

What are parametric solutions for earthquake insurance?

In traditional (indemnity) insurance, the payout is determined by the loss the insured person suffers: the cost of a new windshield after a tree impales it, the price tag for an ambulance ride, or the cost of damage to a home after an earthquake. But determining monetary losses can be slow and fraught — not something individuals or insurers want to deal with after a disaster.

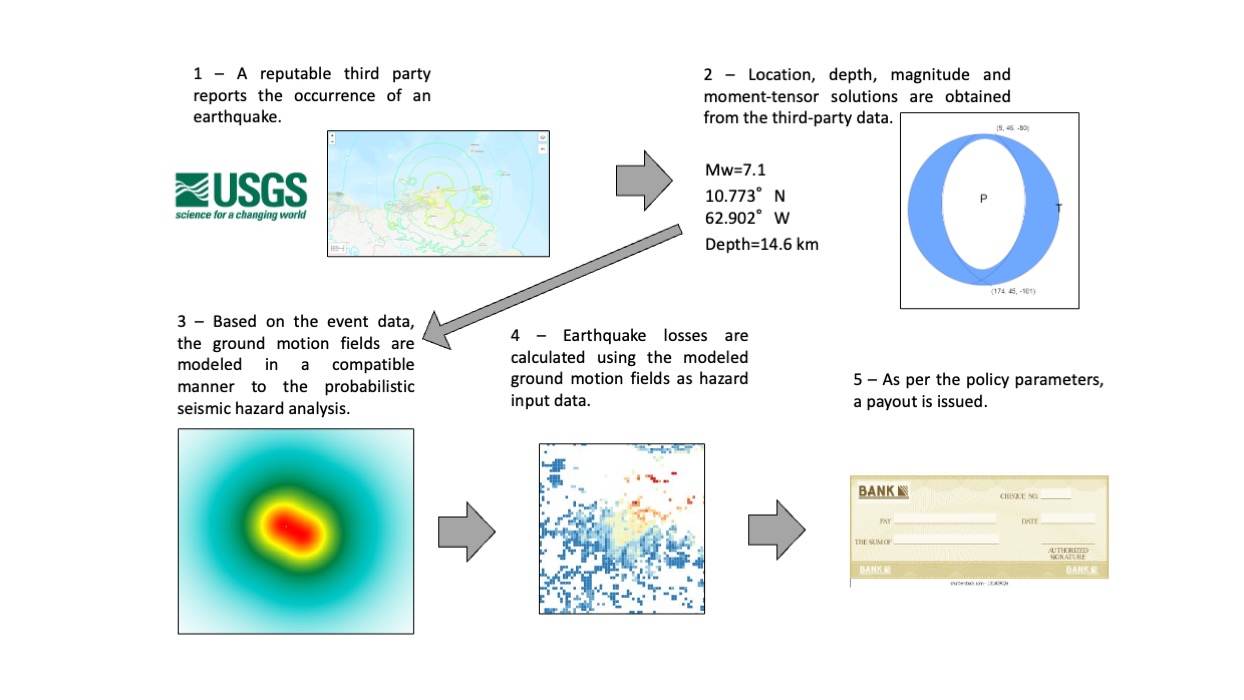

In parametric insurance solutions, the parameters (hence the term “parametric”) that determine a payout are set before the disaster ever occurs. This is accomplished by analyzing key measurable and reliable parameters that correlate well with observed losses in past disasters. For example, for earthquake-related insurance claims, the quake’s magnitude, location and depth as reported by reputable third-party institutions, such as the U.S. Geological Survey (USGS), can be reliably used to calculate payouts.

Parametric insurance solutions can offer multiple advantages. They can be cheaper for the insured individual because there is no loss adjustment process. It also makes the process cheaper for the insurance company because no claims adjustor comes to a damaged building or other asset to perform an on-site investigation. In addition, payouts are rapid, typically received within days after the disaster. And parametric insurance solutions are flexible and customizable, both in setting up what triggers a payout and how severe an event needs to be to result in a certain level of payout.

Payout structures and triggers

Structures. The policies’ flexibility is set using a payout function, which is an equation that describes what fraction of a total potential payout is due. The figure below compares three examples of payout structures to indicate how different policyholders might prefer to balance risk and payouts. One might prefer to use a single threshold that yields a full payout, as in Structure 1, whereas others might prefer to have a nuanced scheme with multiple thresholds, so that a less damaging event will give a small payout as in the case of Structure 3, or smoother transitions between the minimum and maximum payouts as shown in the linear function of Structure 2.

The definition of the thresholds and the amount of the payouts have direct relationships with the insurance premium and, therefore, are sought to be aligned with the interests of the insured. For instance, if the threshold for payout is low and the payout value is high, the premium will be more expensive, so the insured parties can choose the most appropriate thresholds based on their budget.

Triggers. Parametric insurance solutions come into play only when they are “triggered.” There are different types of triggers for parametric insurance policies, and they vary in complexity. Triggers could be a certain magnitude of an earthquake, for instance, or the location of its epicenter. These are the simplest triggers, denoted as “first generation” triggers because only one parameter determines payout in such policies.

Other policies use more complicated “second generation” triggers, including modeled or recorded ground accelerations at one or more sites. In the U.S., where several companies offer parametric insurance for earthquakes, these data are often sourced from USGS ShakeMaps.

The most complex “third generation” triggers, are based on “modeled losses.” Modeled losses come from complete catastrophe risk models, which are typically based on four modules that each contribute one component: hazard, exposure, vulnerability and loss. Hazard refers to the long-term relationship between ground shaking intensity and how frequently these intensities are exceeded. Exposure refers to the characterization of assets on which losses can be inflicted by an event at a specific location. Vulnerability relates to the expected loss with a hazard intensity measure (e.g., ground acceleration). Finally, loss is typically represented through relationships that indicate how often given loss values are exceeded (denoted as exceedance probability curves).

Development and operation of parametric insurance policies for sovereign risk

Catastrophe risk models — needed for the third-generation triggers — are increasingly able to handle the complex demands of parametric insurance solutions. This is particularly important for emerging economies whose insurance markets are not yet well developed. For these insurance markets, parametric insurance solutions offer an effective way of coping with damages from large disasters, decreasing the likelihood that initial earthquake losses will evolve into larger-scale economic or humanitarian crises.

For that reason, some national governments use parametric earthquake insurance solutions. In the Caribbean and Latin America, the CCRIF constituted the first multi-country risk pool in the world. In 2007, CCRIF started offering coverage in the form of parametric insurance for different hazards, including earthquakes, to member countries. Member countries can choose between different payout structures for each of the hazards according to their risk tolerance and what their other options are to financially manage disaster and disaster risk. CCRIF pays out within 14 days of the event, limiting a country’s financial burden after devastating events by quickly providing liquidity to finance the government’s initial stages of disaster response.

CCRIF’s total payouts to date have been approximately $260 million, approximately $50 million of which were due to earthquakes. From the national governments’ perspective, these instruments are an attractive option that allow them to avoid the long process of loss adjustment for assets that are distributed over large territories.

The trigger for CCRIF’s earthquake parametric policies is the most complex, “third generation” option: modeled losses at a countrywide level. It requires the development of earthquake hazard, exposure, vulnerability and loss modules for the long-term estimation of risk in the study area to price the policies.

Updating the model for Caribbean and Central American countries

In our recent study in the Bulletin of the Seismological Society of America, we provide critical updates to the CCRIF’s earthquake model that underpins the parametric insurance policies for member countries. The model generates new probabilistic earthquake hazard and loss estimates at the national level for 34 countries in the Caribbean and Central America.

We use R-CRISIS (Ordaz et al., 2021), a computer program based on a classic probabilistic seismic hazard analysis (PSHA) (Esteva, 1967; Cornell, 1968) to create our earthquake hazard model. The main outcome is a stochastic event set (Salgado-Gálvez et al., 2023) that is used to estimate the earthquake losses in a fully probabilistic manner (Ordaz, 2000). For each country, we developed an exposure database for multiple sectors, such as residential, commercial, industrial, and public buildings, as well as important infrastructure such as power and water distribution systems, ports, airports, and transportation, among others. For each type of asset, we generated an earthquake vulnerability function to provide a continuous and quantitative relationship between ground motion and direct losses. The main outputs of the earthquake risk assessment are exceedance probability curves, which provide a relationship between the loss values and their occurrence frequencies. These curves, one for each country, are the basis for defining the payout structures and premiums of each policy.

Additionally, we developed a post-event tool that automatically estimates the modeled loss and indicates whether a payout is due, as per the policy conditions for each country. Since the USGS typically reports two moment tensor solutions for moderate and large earthquakes, the system chooses the most appropriate one based on a set of simple rules that guarantee the coherence with the probabilistic seismic hazard analysis (Salgado-Gálvez et al., 2020).

Providing the funding for disaster aftermath

All parametric insurance policies are underwritten in a manner analogous to the traditional insurance policies. From an operational perspective, parametric instruments require a calculation agent, which must be an independent and well-reputed party that monitors and calculates payouts as long as a policy is active. It is a common practice that the developers of the earthquake hazard and risk models act as calculating agents in the contracts where their data are used. For ensuring the correct operation of the payout computation process, a verification agent is also included in the process with the responsibility of checking that the payout computations are consistent with those of the calculation agent.

The use of parametric insurance policies can mean the difference for policyholders between a rapid and known payout and waiting for months after a disaster and a loss adjustment process. For businesses, payouts can provide rapid liquidity to compensate for not only damages but also business interruption. For governments, parametric insurance policies are an innovative instrument to complement existing disaster risk financing strategies that can provide the resources to cope with the cost of the most urgent and in some cases, life-saving tasks.

References

Cornell, C. A. (1968). Engineering seismic risk analysis. Bulletin of the Seismological Society of America. 58(5):1583-1606.

Esteva, L. (1967). Criterios para la construcción de espectros de diseño sísmico (in Spanish), Proceedings of the 3rd Pan-American Symposium of Structures Caracas, Venezuela.

Ordaz, M. (2000). Metodología para la evaluación del riesgo sísmico enfocada a la gerencia de seguros por terremoto, Universidad Nacional Autónoma de México. Mexico City, Mexico.

Ordaz M., Salgado-Gálvez M. A., Giraldo S. (2021). R-CRISIS: 35 years of continuous developments and improvements for Probabilistic Seismic Hazard Analysis. Bulletin of Earthquake Engineering. 19:2797-2816.

Salgado-Gálvez M. A., Ordaz M., Huerta B., Singh S.K., Pérez-Campos X. (2020). Simple rules for choosing fault planes in almost real-time post-earthquake loss assessments. Natural Hazards. 104(1):639-658.

Salgado-Gálvez M.A., Ordaz M., Singh S.K., Pérez-Campos X., Huerta B., Bazzurro B., Fagà E. (2023). A Caribbean and Central America Seismic Hazard Model for Sovereign Parametric Insurance Coverage. Bulletin of the Seismological Society of America. 113(1):1-22.

- When Tokyo’s next big earthquake hits, could global markets crash? - March 20, 2026

- The Earthquake that Shook the South - February 26, 2026

- Introducing Coulomb 4.0: Enhanced stress interaction and deformation software for research and teaching - February 20, 2026