A 30-year-old assessment warns that a major Tokyo earthquake could crash global financial markets. Whether this holds comes down to key decisions made under pressure, according to a 2022 report.

By Lauren A. Koenig, Ph.D., Science Writer

Citation: Koenig, L., 2026, When Tokyo’s next big earthquake hits, could global markets crash?, Temblor, http://doi.org/10.32858/temblor.374

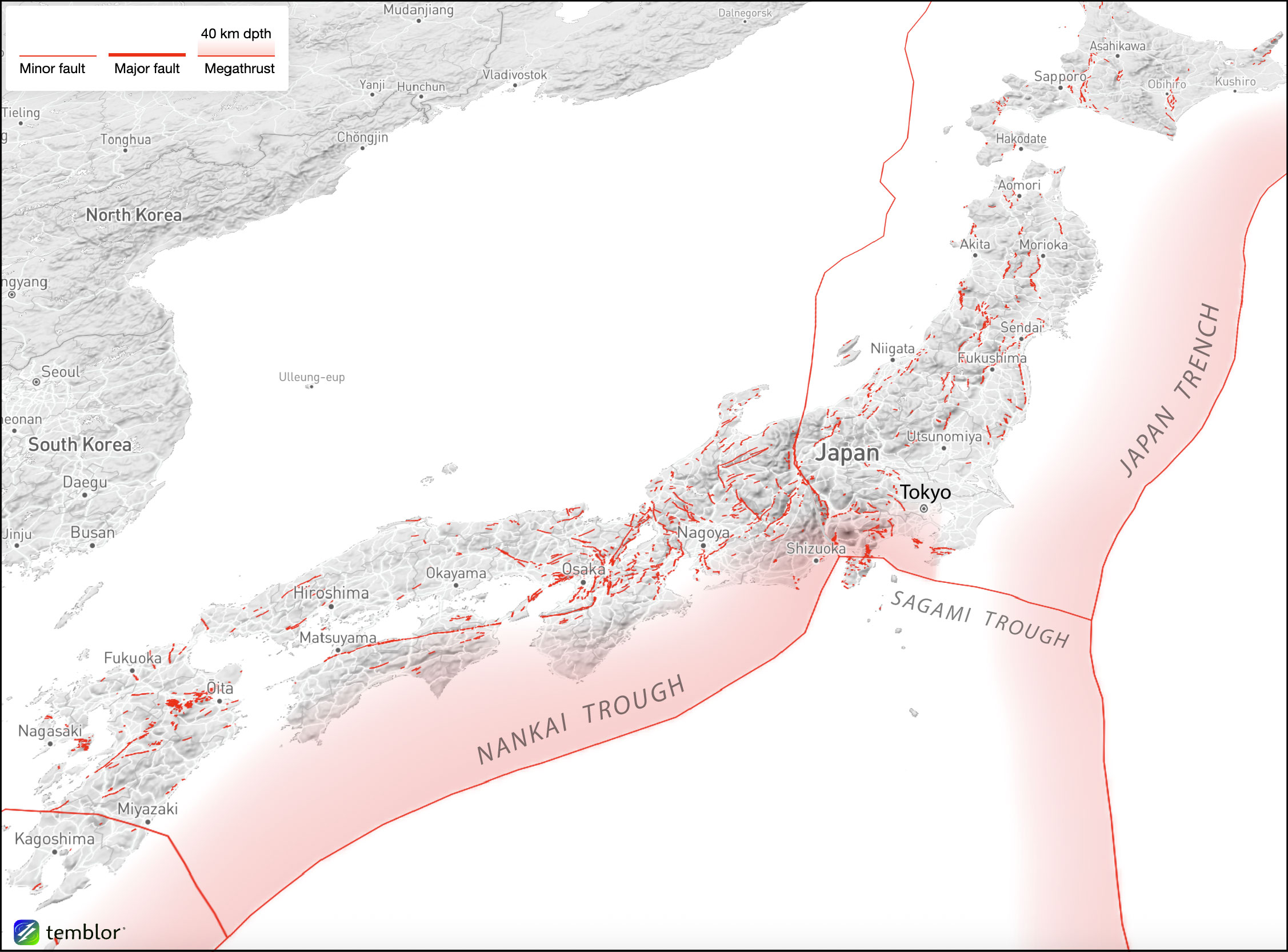

Japan experiences thousands of earthquakes each year, some of which have become defining disasters of modern history — from the devastating 1923 Great Kanto earthquake and ensuing fires to the 2011 magnitude 9.1 Tohoku earthquake and tsunami.

Although the physical devastation from such events is well documented, the potential for global financial fallout has been overlooked. In 1989 and 1991, financial analyst Michael Lewis and journalist Peter Hadfield separately warned that a major Tokyo earthquake could trigger a worldwide stock market crash. They described a specific chain reaction: Japanese banks would raise emergency cash by selling foreign securities (their holdings of stocks and bonds issued by U.S. and European companies and governments), flooding U.S. and European markets with sell orders and sending prices tumbling globally — all while Japan’s own markets remained closed.

Then, for three decades, the financial world appeared to largely forget about their warning.

A 2022 report by Nigel Winspear for CATRISX SERVICES revisited this prediction with updated financial modeling and confirmed that the risk remains real. Winspear’s analysis identified different scenarios in which inadequate earthquake insurance, massive reconstruction costs, and Japanese banks’ $659 billion in foreign securities could create a pathway for a major Tokyo earthquake to trigger a global market crash.

Japan faces a high probability of another major earthquake; the government estimates a 70% probability of a magnitude 7 event or larger within 30 years. If a large enough quake strikes the wrong place at the wrong time, the world’s interconnected markets could face an unprecedented test. Whether this triggers worldwide financial consequences depends on decision-makers acting effectively under extreme stress.

Where wealth meets the fault line

What makes Tokyo different from other earthquake-prone cities comes down to an unusual convergence of geology and economics. The Tokyo Metropolitan Area and surrounding Kanto region generate about 40% of Japan’s GDP. If it were a standalone country, Kanto would rank within the world’s top-ten largest economies, on par with Canada and Brazil. The region’s wealth density is staggering — more than five times that of Silicon Valley, according to Winspear’s report.

This concentration of economic power sits atop one of the most seismically active zones on Earth. Japan lies at the junction of four major tectonic plates: the Pacific, Philippine Sea, Eurasian, and North American plates. This convergence generates more than 1,000 earthquakes of magnitude 4 or higher each year. Most are minor, but catastrophic events remain a constant threat.

Modeling the range of risk

Winspear’s report modeled three Tokyo earthquake scenarios with dramatically different economic consequences: a magnitude 7.3 earthquake similar to the one that destroyed Edo (Tokyo’s predecessor) in 1855; a magnitude 7.9 earthquake similar to the 1923 Kanto quake; and an even larger potential earthquake exceeding magnitude 7.9.

The first and most likely earthquake scenario wouldn’t cause a worldwide financial crisis. A magnitude 7.3 earthquake has a 70% probability of occurring in the next 30 years. Such an event would be locally devastating; the Japanese government estimated that a similar event could destroy more than 600,000 buildings. However, Japan’s available physical cash should be sufficient to finance rebuilding without massive bank withdrawals, according to the report.

The real concern lies with less frequent but more severe scenarios. Winspear’s report focused on scenario two, the 1923 Kanto-like quake — a magnitude 7.9 event large enough to stress the financial system, yet specific enough to model based on well-documented historical impacts. A 2019 industry catastrophe model suggested a similar event today would cause property damage exceeding $1.5 trillion. Including lost production, damaged infrastructure, and shuttered businesses, Winspear estimated the total economic toll could reach $3.2 trillion — equivalent to 59% of Japan’s GDP in 2019.

Scenario 3, an earthquake exceeding magnitude 7.9 in the Kanto region, could cause property damage surpassing $3 trillion and total economic losses exceeding $4.5 trillion. Although modeled with less certainty due to limited recent historical precedent, this earthquake scenario illustrates how catastrophic financial effects could escalate in response to increasing earthquake magnitude.

The financial projections for these scenarios depend on how many buildings would be damaged and how much of that damage would be covered by insurance. The greater the gap between insured versus uninsured structural damage, the more likely a domestic banking issue could spread to global markets.

These larger-magnitude scenarios are only estimated to reoccur every 180 to 400 years, but would represent the largest economic loss from any natural disaster in history relative to a single developed nation’s economy.

Factoring in modern resilience

Kishor Jaiswal, a research civil engineer at the U.S. Geological Survey, has examined similar scenarios globally. “At first glance these estimates appear very high to me,” says Jaiswal. “But make no mistake, such an earthquake will be the costliest earthquake of our times.”

Jaiswal notes improvements in Tokyo’s urban center, where the infrastructure has changed since 1923. “The population has tripled or more since the 1920s, but the building stock in the urban development is also very different, with a large fraction of the buildings being mid- or high-rises in urban corridors,” he notes. Although damage and some collapses are inevitable, “the vast majority of buildings are expected to survive with some damage,” and Tokyo would not see the same level of fatalities as in 1923.

The broader Tokyo Metropolitan Area presents a more complex picture. About 25% of buildings in the area pre-date the 1981 Building Standard Law, which requires structures to be built to withstand magnitude 7.0 earthquakes. Winspear’s report also considers low-rise residential buildings in the suburbs, which are more at risk both from shaking and fires that could spread after the earthquake. Even buildings left standing may suffer structural damage requiring partial or complete demolition, creating costs that fall largely on uninsured property owners who would need to tap their bank savings.

Jaiswal also expects significant global supply chain disruption. “The repeat of the 1923 sequence will certainly induce sizable disruption on global trade and supply chains,” he says, though he notes the impacts would hopefully be “limited and short-lived” if not exacerbated by tsunami or nuclear issues like those that worsened the 2011 disaster. What distinguishes Tokyo from other earthquake-prone regions is its concentration of corporate headquarters: Most major Japanese companies are based in the metropolitan area, amplifying the potential for global economic disruption.

The $659 billion question

The process by which an earthquake could trigger a global financial disaster centers on a striking detail: As of 2019, Japanese banks held approximately $659 billion in foreign securities — almost matching the $690 billion that Winspear’s report estimated these banks would need to meet withdrawal demands after a Kanto-like magnitude 7.9 earthquake (scenario 2).

The cascade would begin when the earthquake destroys or damages hundreds of thousands of buildings. Earthquake insurance would be of very little help; only about 37% of Tokyo households carry earthquake insurance (although this is roughly triple the amount of residents with earthquake insurance in California), and commercial coverage is often capped at less than 20% of a property’s insured value. This would create what the report describes as the largest “protection gap” of any seismically active region globally.

With insurance covering only a fraction of losses, property owners would turn to their bank deposits to pay for reconstruction. Banks would face a sudden liquidity crunch: Although they should have sufficient assets overall, they wouldn’t be able to instantaneously turn those assets into cash to meet withdrawal demands.

Japan’s stock market would likely immediately close and could remain shut for weeks while residents attend to personal loss and damages. Meanwhile, the domestic bond market — where government and corporate debt is traded, generally considered more stable than stocks — would freeze because the banks that normally buy bonds from each other would be trying to sell instead. That leaves foreign securities as the only readily available option for quickly raising cash.

If Japanese banks moved to sell their entire $659 billion in foreign holdings quickly, foreign markets would face a severe test. Buyers might be scared off by seeing reports of damage to the world’s third-largest economy. Stock markets would be particularly vulnerable. As liquidity dries up (fewer investors are willing to buy shares), stock prices would fall, potentially triggering the kind of global crash Lewis and Hadfield warned about three decades ago.

Insurance and market confidence

Modern financial instruments could help mitigate this risk, according to financial experts. Insurance-linked securities, also called catastrophe bonds, work like bonds with a catch: Investors buy them upfront, essentially betting that a specific disaster won’t occur. In normal years, they receive interest payments. But if the disaster strikes, investors lose part or all of their initial investment, and that money automatically flows to insurance companies or governments to pay claims. This gives insurers access to capital beyond traditional reinsurance (insurance for insurance companies, to protect themselves and transfer some of their risk to other companies).

“The key mitigating impact of ILS [Insurance-Linked Securities] and other financial instruments that spread catastrophe risk is its effect on market confidence,” explains John Seo, co-founder and managing director of Fermat Capital Management. Insurance-linked securities helps ensure that insurance markets can continue operating after a disaster, which matters for reconstruction financing. “If the asset is uninsured, the banks cannot lend against it,” he says. “Post-event, the specter of a closed insurance market can cause financial markets to lose confidence, which in turn can lead to hyper volatility or even a market crash.”

Even though only about 37% of Tokyo households currently have earthquake insurance, what matters for preventing a broader financial crisis is whether insurance remains available at all. If insurance companies can’t pay claims or won’t issue new policies, then reconstruction stops because banks won’t finance rebuilding of uninsured property.

The psychological impact matters as much as the capital itself. “It is not so much the damage itself that is the problem as the forward-looking picture,” Seo explains. If property owners can secure insurance-backed financing and the post-disaster outlook appears manageable, the pressure on banks to sell foreign securities could be significantly reduced.

Critical decisions ahead

A global financial meltdown isn’t an inevitable consequence of a major Tokyo earthquake. The report identifies three critical interventions that could prevent the crisis: emergency loans or bond purchases from the Bank of Japan would give banks the cash they need without having to sell foreign holdings (although this assistance would more likely take weeks to arrive); coordinated intervention by foreign central banks in their own stock markets could stabilize stock prices; or if foreign markets aren’t caught by surprise, sufficient liquidity could remain available to absorb the sell orders.

The challenge is that none of these protections are in place, Winspear noted in his report. The Bank of Japan would need to provide four times more emergency funding than it did during the entire 2008 financial crisis, and it has no responsibility to protect foreign markets. Central banks rarely intervene to support stock markets in other countries, and coordinated global action in this area would be unprecedented.

Yet, Seo offers measured optimism about overall preparedness: “On the principle that financial markets react worse to events that were completely, utterly uncontemplated, I believe that financial markets are more prepared for a major Japanese quake event.” In other words, simply discussing the scenario has made markets less vulnerable than three decades ago.

The 30-year-old warnings identified a genuine vulnerability that remains relevant today and Winspear’s report shows preparation measures are not yet realized. Whether markets crash or hold steady may come down to whether decision-makers, including those who may themselves be injured or displaced by the disaster, respond effectively in the critical days following a major earthquake in Japan.

References

Winspear, N. (2022, January 11). Tokyo earthquake: Possible impacts on the global financial markets. CATRISX SERVICES LTD.

Copyright

Text © 2026 Temblor. CC BY-NC-ND 4.0

We publish our work — articles and maps made by Temblor — under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International (CC BY-NC-ND 4.0) license.

For more information, please see our Republishing Guidelines or reach out to news@temblor.net with any questions.